Risk shows up in real estate long before it appears in a valuation report. A neighborhood can change. A drainage issue can turn into recurring flood losses. A new road project can improve accessibility or bring noise and safety concerns. For risk analysts, underwriters, and real estate developers, the challenge is not “finding data.” It is finding the signals that move early and then turning them into decisions.

That is where real estate risk assessment data powered by alternative sources becomes useful. Traditional inputs like comps, historical prices, and basic demographics remain important, but they often miss fast-moving, local risks. Alternative data fills that gap with a wider view of property risk data, from flood exposure and severe weather history to crime, school context, news signals, and even early financial stress indicators that affect credit risk property outcomes.

This guide breaks down the most practical alternative datasets, how teams collect them (including environmental risk scraping), and how to combine them into a model you can actually use for underwriting and development planning.

Why alternative data matters in property risk

Traditional risk assessment tends to be backward-looking. It relies on what happened before at a broad-area level. Alternative data is different. It is more granular, more current, and often closer to the real drivers of loss and value volatility.

A practical way to think about it is this:

- Traditional data explains “what the market did.”

- Alternative data explains “what the property is exposed to next.”

When you bring both together, your risk decisions become more defensible, especially for borderline deals where one hidden factor can swing outcomes.

What counts as alternative property risk data

Alternative data in real estate usually falls into five buckets:

1) Environmental and climate exposure

Flood hazard, storm history, heat and air quality, wildfire proximity, seismic exposure, soil and drainage signals.

2) Neighborhood and livability signals

Crime trends, school context, transit changes, noise corridors, and major development projects.

3) Local change detection

News and public updates about zoning shifts, infrastructure work, litigation, community opposition, or pollution issues.

4) Financial stress signals

Delinquencies, foreclosure pressure, rent-payment stress proxies, local employment shocks, and rate sensitivity.

5) Digital sentiment and “early warnings.”

Community complaints about flooding, construction quality, power outages, water issues, safety, or governance.

You do not need every bucket for every use case. Underwriting often starts with environmental, neighborhood, and credit factors. Developers often start with environmental + local change detection.

Scraping flood zone and weather risk data

Environmental risk is one of the easiest places to add immediate value because it is measurable and strongly linked to losses.

Flood zones and flood hazard layers

In the U.S., FEMA’s National Flood Hazard Layer (NFHL) provides current, effective flood hazard data as a geospatial dataset. FEMA’s Flood Map Service Center is commonly used to access official flood maps and related flood hazard products.

What this gives you in practice:

- flood zone classification by location

- a baseline to flag properties that need deeper flood review

- a consistent layer you can join to parcels or coordinates

Severe weather history and event narratives

NOAA’s Storm Events Database contains records of severe weather events collected by NOAA’s National Weather Service (NWS) and includes long historical coverage. For live alerts and forecasts, the NWS also provides an API that exposes this data.

What this enables:

- frequency and severity of storm exposure by county/region

- “event types that matter” for your portfolio (hail, tornado, heavy rain, heat)

- alerts that can trigger portfolio monitoring or site checks

Earthquake exposure

If you underwrite in seismic regions, the USGS provides an Earthquake Catalog API for querying earthquake events. Even when you are not building a full seismic model, this helps add a factual exposure layer for certain geographies.

Collecting crime and school ratings for neighborhood risk

Environmental exposure explains “what nature can do.” Neighborhood signals explain “what the market and community conditions can do.”

Crime risk signals

For U.S.-based analysis, the FBI’s Crime Data Explorer provides access to law enforcement crime data, and the FBI Crime Data API offers a read-only service that returns crime data in JSON or CSV formats.

How teams use it:

- Build a “crime trend index” over time, not just a single snapshot

- Compare micro-areas (ZIP, precinct, or radius buffers where possible)

- Separate violent vs property crime, because they affect demand differently

School context

School quality is a strong driver of demand in many markets. NCES is the U.S. federal statistical agency for education data, and it also provides open-data API access through its platform.

How teams use it:

- Link properties to nearby school options

- Track changes in enrollment, programs, or district-level signals

- Use as a stability indicator for long-term demand pockets

Monitoring news for neighborhood changes

Some risks do not come from nature or long-term social patterns. They come from sudden local changes: policy decisions, protests, zoning approvals, industrial incidents, or infrastructure disruptions.

A practical way to monitor this at scale is using structured news datasets. For example, GDELT monitors global news coverage across languages and supports searching and analysis over that coverage.

What to look for:

- New infrastructure projects (positive or disruptive)

- Legal disputes involving large developments

- Pollution incidents or regulatory actions

- Community opposition can delay projects

- Recurring reports of flooding, fires, or outages in a locality

The goal is not to read every headline. It is to catch “risk-changing events” early.

Using social media for emerging risk signals

Social posts and local forums are often where early warnings first appear: “this area floods every monsoon,” “new construction has water issues,” “frequent power cuts,” “unsafe after 9 PM,” “builder delays.”

If you use social listening, keep it practical:

- Focus on themes (flooding, safety, delays), not individuals

- Aggregate at the neighborhood or project level

- Apply strict privacy and platform-rule hygiene

This is especially useful for developers during site selection and for underwriters when a location is borderline.

Credit risk property indicators that improve underwriting

Property risk is not only physical. It is also financial.

Depending on your market, useful credit and affordability signals include:

- Rate sensitivity (how quickly demand drops when rates rise)

- Rent-to-income stress proxies in micro-markets

- Foreclosure and distress signals (where available through lawful sources)

- Tenant stability signals for income properties

This is where credit risk property analysis meets location intelligence. Two properties with the same “value” can behave very differently under stress scenarios, depending on the surrounding affordability and liquidity.

Combining diverse data in risk models

Alternative data only becomes valuable when it is standardized and comparable.

Step 1: Normalize everything to the same keys

Most teams standardize around:

- Geography (lat/long, parcel ID, ZIP, tract, radius buffers)

- Time (weekly/monthly snapshots)

- Source versioning (so you know when something changed)

Step 2: Convert raw signals into features

Examples:

- Flood exposure class + distance to floodplain boundary

- Storm event frequency in the last N years

- Crime trend slope (improving vs worsening)

- “School stability” proxy

- Negative news spike index

- Social complaint intensity by theme

Step 3: Build a risk score that matches your decision

A simple scoring approach often works better than an overfitted model early on.

For example:

- Environmental risk: 40%

- Neighborhood risk: 25%

- Liquidity/market stability: 20%

- Financial stress proxies: 15%

Then backtest against outcomes you care about:

loss ratios, default rates, vacancy spikes, price drawdowns, and project delays.

Step 4: Monitor drift

Alternative data changes. Websites change. Local dynamics change. Models can silently degrade. Drift monitoring (and source monitoring) keeps your score trustworthy.

Operationalizing risk signals

Once the model is stable, the best teams turn it into workflows:

- Underwriting checklist triggers (extra review when flood + negative news spike)

- Developer site ranking dashboards

- Automated alerts for new risk events in a neighborhood

- Portfolio monitoring by risk tier

If your organization already has “monitoring DNA” from other domains, this becomes even easier. For example, teams that already monitor Amazon Marketplace data for price volatility and listing health often adopt the same alert-and-dashboard mindset for property risk signals.

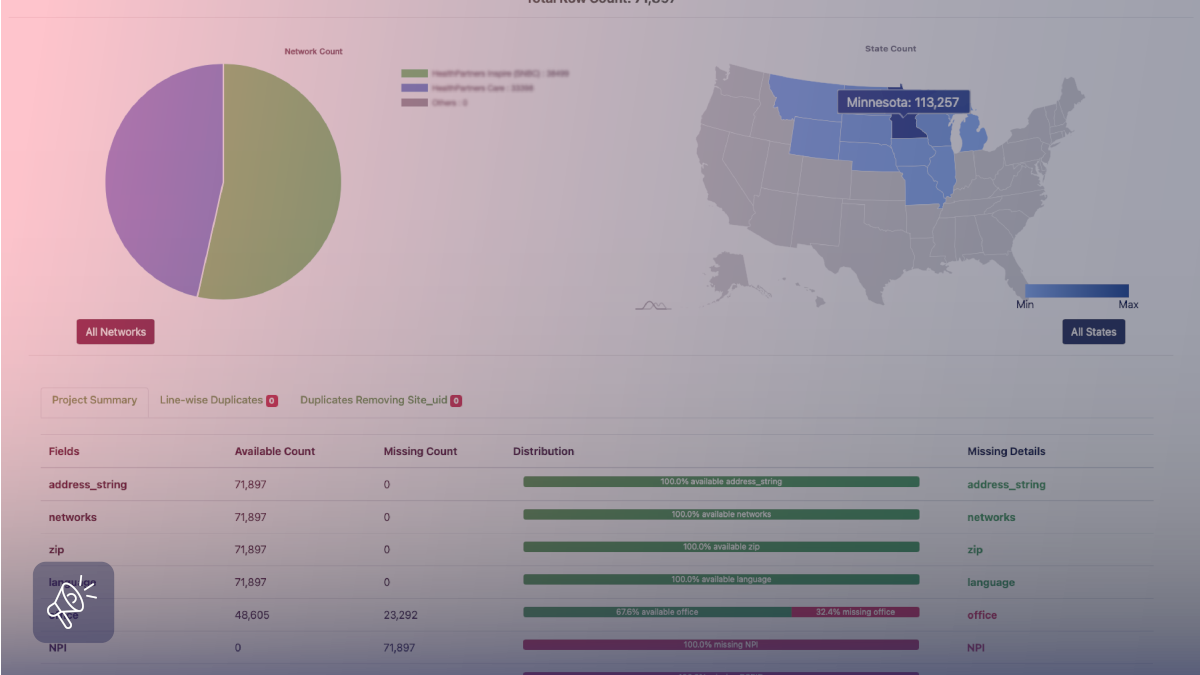

How Grepsr supports alternative data for property risk assessment

Alternative data projects usually fail for one boring reason: the pipeline breaks. A permit portal changes its layout, a county site updates formats, and suddenly your schema drifts. Then, analysts spend more time fixing extraction than on modeling risk, and the risk score starts to lag behind reality.

Grepsr keeps the plumbing stable by delivering web and public-record datasets as a managed feed, with custom extraction, validation, and refresh cycles that you can run on a schedule or on demand. In one real estate intelligence use case, Grepsr provides state-wise property and building permit data to support risk assessments and valuations without the usual delays when sources change.

And when your workflow starts looking more like underwriting, the same idea applies: you need fresh external signals in a consistent structure. Grepsr’s Agentic Insurance customer story shows how structured web data can power risk indicators within AI-driven decision systems, rather than remaining scattered raw inputs.

Conclusion

Property risk is multi-dimensional. A good decision needs more than last year’s comps.

When you combine real estate risk assessment data with alternative signals like flood exposure, severe weather history, neighborhood crime and school context, and emerging news and social risk indicators, you get a clearer picture of what could go wrong and what could change next. For underwriters, that means fewer surprises. For developers, it means better site decisions. For risk teams, it means a model that reflects reality rather than averages.

FAQs: Real Estate Risk Assessment Data

What is alternative data in real estate risk assessment?

Alternative data is information beyond traditional comps and demographics, such as flood hazard layers, storm history, crime trends, school context, news signals, and social sentiment that can impact property performance.

How do I scrape flood zone and weather risk data?

Many teams use authoritative datasets like FEMA flood hazard layers and NOAA severe weather records, then join them to property locations. FEMA provides NFHL flood hazard data and official flood maps through its tools.

Where can I find reliable severe weather event data?

NOAA’s Storm Events Database provides records collected by the National Weather Service, and the NWS offers an API for forecasts and alerts.

What sources can I use for crime and school context?

In the U.S., crime data can be accessed via the FBI Crime Data Explorer and its Crime Data API. Education datasets and APIs are available through NCES.

Can news and social data really improve risk models?

Yes, as an early-warning layer. News databases like GDELT help monitor neighborhood-changing events, while social listening can surface recurring on-the-ground issues earlier than formal reports.